Rising Property Taxes & Insurance in Michigan: The Hidden Costs Buyers Overlook When Qualifying for 2026 Loans

Why Standard Mortgage Calculators Fall Short for Michigan Homebuyers

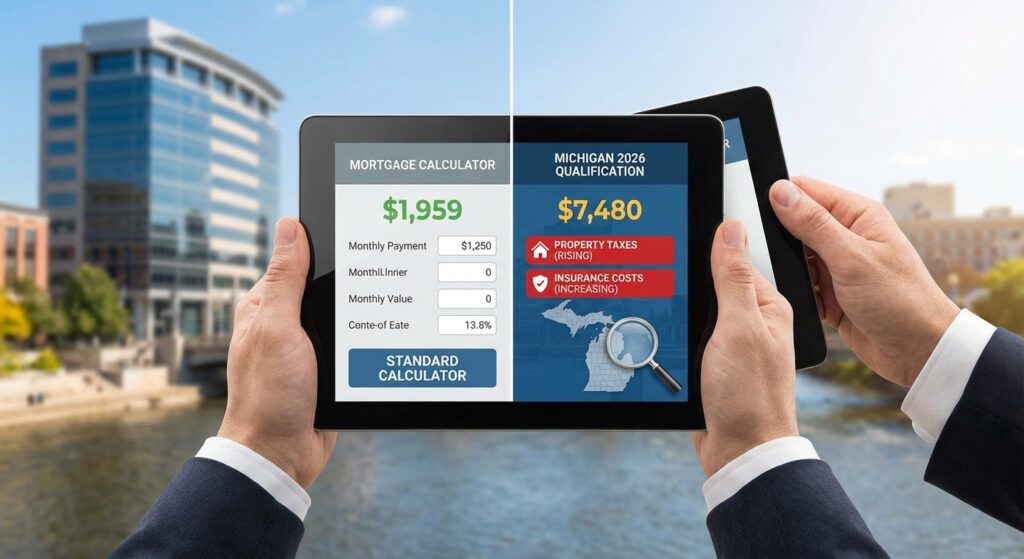

When planning to buy a home in Grand Rapids, Michigan, relying on a generic online mortgage calculator can lead to a rude awakening. Most standard calculators focus heavily on principal and interest but fail to account for the true cost of homeownership in our state. As we approach 2026, advanced loan qualification requires a deeper understanding of Michigan specific financial burdens, such as fluctuating millage rates, increasing wind and hail risks, and updated flood zone designations.

At Priority Home Mortgage, our expert team helps buyers navigate these hidden costs. If you do not factor in local tax uncapping and rising insurance premiums, your actual monthly payment could inflate hundreds of dollars beyond what a basic calculator estimates. We specialize in real estate financing from first-time homebuyers to avid investors, ensuring your Home Purchase Loan is structured around reality, not just base estimates.

Decoding Michigan Millage Rates and Insurance Premiums

To accurately calculate your housing budget, you must factor in the unique elements of Michigan property taxes and homeowners insurance. Here is exactly what you need to know before you start house hunting:

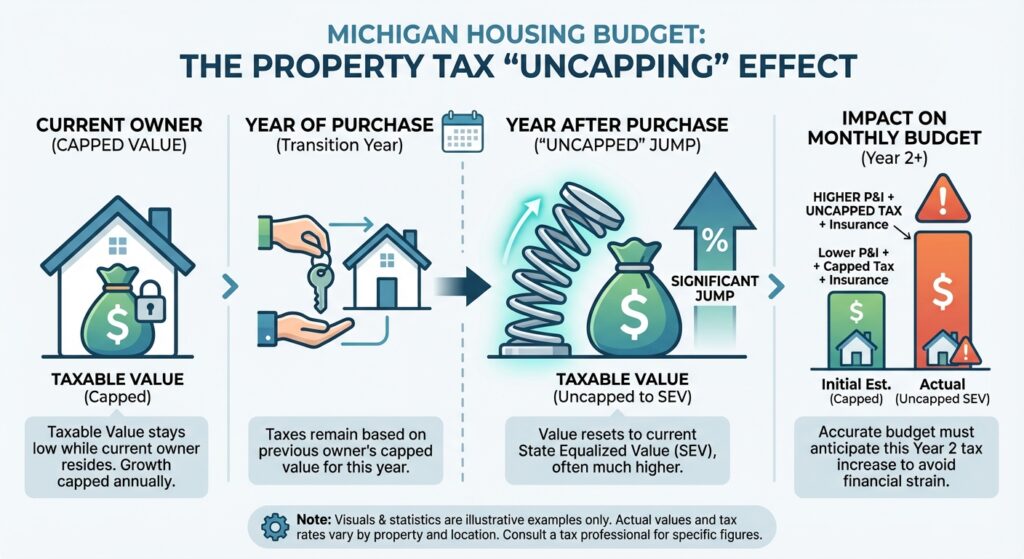

- The Uncapping of Property Taxes: Under Michigan law, a property’s taxable value is capped while the current owner lives there. However, the year after you purchase the home, the taxable value uncaps and adjusts to the current State Equalized Value (SEV). This can cause a significant jump in your tax bill that standard calculators miss completely.

- Local Millage Rates: Grand Rapids and surrounding West Michigan communities have specific millage rates that fund local schools, libraries, and emergency services. These rates vary drastically even between neighboring zip codes.

- Weather-Related Insurance Risks: Severe weather, including intense windstorms and hail, has driven up insurance premiums across the state. Many policies now include separate, higher deductibles for wind and hail damage, which increases your overall escrow requirements.

- Flood Zone Reclassifications: As weather patterns shift, FEMA is updating flood maps. Homes previously outside of high-risk zones may now require expensive flood insurance policies, which can heavily impact your debt-to-income ratio for Conventional Loans or FHA Loans.

Working with a local Grand Rapids mortgage lender ensures these factors are calculated properly before you make an offer.

| Cost Component | Standard Calculator Estimate | True 2026 Michigan Estimate |

|---|---|---|

| Principal & Interest (P&I) | $1,800 | $1,800 |

| Property Taxes (Monthly) | $250 (Based on old capped value) | $450 (Based on uncapped SEV & local millage) |

| Homeowners Insurance | $80 | $160 (Includes wind/hail riders) |

| Flood Insurance | $0 | $75 (If reclassified by FEMA) |

| Total Monthly Payment | $2,130 | $2,485 |

How Priority Home Mortgage Protects Your 2026 Housing Budget

Preparing for a home purchase in 2026 means looking beyond the sticker price. Whether you are a first-time homebuyer or an experienced investor, Matthew Peterson and the team at Priority Home Mortgage are dedicated to providing advanced qualification services. We run the actual numbers based on the specific Grand Rapids neighborhood you are targeting, factoring in exact millage rates and consulting with local insurance agents to estimate accurate premiums.

By securing a comprehensive pre-approval, you avoid the shock of a payment that inflates beyond your comfort zone. If you are exploring VA Loans, Jumbo Home Loans, or even looking to Refinance an existing property to manage rising costs, our highly experienced loan officers will tailor a financial solution to meet your exact needs. We pride ourselves on offering some of the most competitive rates nationwide while making the loan process simple, straightforward, and fast.

Q1: Why do Michigan property taxes increase after buying a home?

Due to Michigan’s Proposal A, a property’s taxable value is capped for the current owner. Once the property is sold, the taxable value uncaps the following year to match the current assessed value, which often results in a significantly higher tax bill for the new buyer.

Q2: What is a millage rate and how does it affect my mortgage payment?

A millage rate is the tax rate used to calculate local property taxes. One mill equals one dollar per $1,000 of taxable property value. Higher millage rates in certain Grand Rapids neighborhoods will increase your monthly escrow payment.

Q3: Why are home insurance rates rising in Michigan for 2026?

Insurance companies are adjusting premiums to account for increased claims related to severe weather events, specifically wind and hail storms. Higher replacement costs for building materials also contribute to these rising rates.

Q4: Will I need flood insurance if I buy a home in West Michigan?

It depends on the property’s specific location and the latest FEMA flood maps. If the home is located in a designated high-risk flood zone, your lender will require you to carry a separate flood insurance policy.

Q5: How can Priority Home Mortgage help me avoid payment shock?

Our Grand Rapids mortgage experts use advanced qualification methods to factor in uncapped taxes, accurate millage rates, and realistic insurance premiums. This ensures your pre-approval reflects the true cost of homeownership before you sign any paperwork.

Ready to find your true purchasing power?

Don’t let hidden costs derail your homeownership dreams.